New Regulatory Measures for Borderless Investment

Perhaps unbeknownst to the locals, Hong Kong is already entering the Web 3.0 era. Not only has the SAR Government been actively promoting its development in recent years, but in May 2024, Cyberport also announced the establishment of the “Web 3.0 Investors Circle” under Cyberport Investors Network to facilitate related investment. These progressive initiatives hinge on web security and protection for online consumers and investors.

How will the advent of Web 3.0 impact the ways people live and invest? The virtual-asset market is the holy grail for financial cities around the globe. With its status as an international financial centre, Hong Kong is set to secure its place in the market. In addition to supporting the sector’s development, the SAR Government, for its part, should formulate a custom-made regulatory framework.

Beware of virtual-investment traps

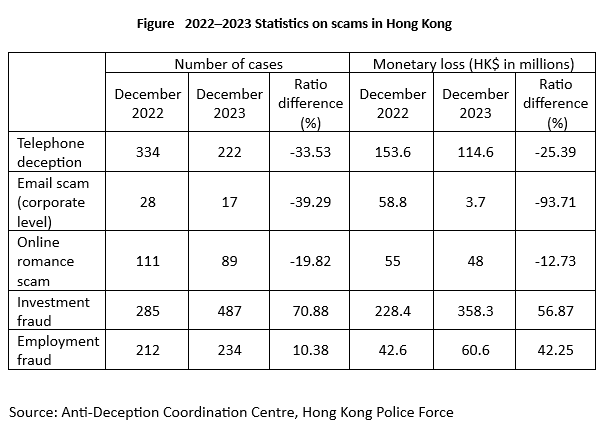

Virtual assets are part and parcel of the Web 3.0 ecosystem. Recent years have seen an upward trend of virtual-asset scams. Data for December 2023 of the Anti-Deception Coordination Centre of the Hong Kong Police Force illustrates that the top three most common investment frauds are investment fraud, employment fraud, and telephone fraud, with investment fraud showing a soaring rate of increase (see Figure).

The recent occurrence of a series of serious fraud cases in the virtual-asset market has been cause for alarm for some investors. The massive financial fraud case involving JPEX in 2023 turned out to be a crash course in virtual-asset investment for Hongkongers. The Securities and Futures Commission thus regularly publishes a list of suspicious virtual-asset trading platforms and a list of service providers applying for a licence to operate a virtual-asset trading platform.

Advantages of new financial products

On a traditional financial market, investment activities rely on interpersonal interaction. In order to avoid imitation by competitors, companies have the right to refuse disclosing details of their business models, leading to asymmetric information. Owing to high-efficiency operations and complexity of the modern-day financial market, it is necessary to integrate contractual trust into investment relations, which is the trust in the other party to fulfil their contractual obligations. A contract enables investors to accurately evaluate risks and returns, assisting all parties in assessing risks, including potential profits and losses of trustees.

The rapid advancement of technology has also brought about earth-shattering changes to the financial sector. As an emerging financial technology, decentralized finance (DeFi) can provide financial services without relying on traditional financial intermediaries, offering more cost-effective and safer alternative solutions to the conventional financial system. DeFi retains various traditional financial services, including exchange, lending, insurance, and asset management, yet it is unbeholden to any central authority. In addition, the trust mechanism of DeFi is based on smart contracts, which are program codes used to formulate contracts. By minimizing costs and potential human errors, it helps to address inadequacies of the conventional financial system.

Overnight change from summer to winter

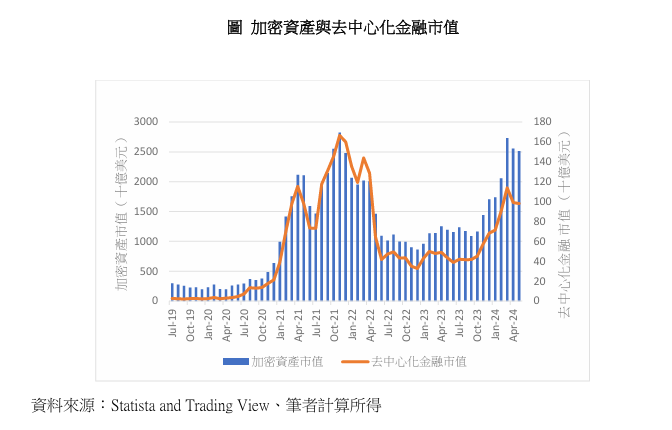

Thanks to high expected returns and flexible investment options, DeFi became the fastest growing sector of crypto assets from 2020 to 2021, referred to as the “DeFi Summer”. The market capitalization of DeFi products and services skyrocketed from US$4.5 billion in June 2020 to US$166.5 billion in November 2021, marking a historical high. Meanwhile, the total number of crypto-asset wallets leaped from about 200,000 to around 5 million (see 【Note 1】).

However, the bankruptcy of major crypto-asset service providers one after another revealed how easily retail investors could be lured by the promise of unrealistically substantial returns. The complete anonymity of cryptocurrencies makes them exploitable by criminals, progressively exposing the underbelly of the market. As a consequence, the negative shift in investor sentiment ushered in the “Crypto Winter”.

The price of crypto assets plummeted by 75% from the peak in late 2021 while Defi’s market capitalization fell to US$32 billion by the end of 2022 (see Figure). Nevertheless, DeFi so far represents but a relatively small portion within the crypto-asset ecosystem. With its market value standing at US$113.7 billion as of March 2024, DeFi merely accounted for 4.1% (US$2.73 trillion) of the total market capitalization of crypto assets.

Figure Market capitalization of crypto assets and DeFi

Source: Statista and Trading View; authors’ calculations

Inherent flaws and potential risks of DeFi

There is evidently a lack of comprehensive investor-protection measures for the DeFi market. While DeFi and the crypto-asset market have been undergoing rapid growth, regulatory measures have yet to be standardized across countries because of their cross-border nature. Characterized by its access to high leverage from lending and trading platforms (see 【Note 2】), DeFi enables investors to purchase more assets after making an initial investment. However, when it becomes necessary to decrease the debt, due to investment loss or collateral depreciation, investors would be forced to sell their assets, exerting further downward pressure on prices. That explains why investors suffered huge losses when the DeFi market crashed in 2022.

At the same time, the cross-border nature of blockchain has also given rise to compliance and legitimacy issues while there is a lack of cohesion in legislation and law enforcement in different jurisdictions. The worldwide nature of DeFi and the crypto-asset market means that DeFi entities, participants, and related activities often straddle national borders, with varying rigidity of regulatory standards among them. Operators and service providers failing to comply can thus seek to take advantage of loopholes and relocate to countries with minimal or zero regulation. This also makes it difficult for financial institutions to gather relevant information, posing a big hurdle to investor protection.

The absence of standardized definitions and classifications of crypto assets has created enormous challenges for the world’s financial regulators in analysing and verifying the authenticity of different crypto-assets products. Given the immutability of smart contracts, any errors or loopholes in the contract’s programming code could have dire consequences. Besides, legal recourse is elusive in the event of disputes derived from financial smart contracts.

Regulatory approaches and investor protection

With regard to DeFi and the entire virtual-asset market, financial authorities around the world are upholding the principle of “same activity, same risk, same regulation”. By affording the same treatment to business activities of the same nature and with the same risk, this practice ensures fair competition for all companies. Governance issues often arise with DeFi agreements which claim to be decentralized but are in fact centralized, resulting in false claims and moral hazards. All DeFi platforms have a central management framework which outlines how to formulate strategies and operational priorities. The centralized element, based on governance token holders (usually platform developers), can serve as the basis for recognizing DeFi platforms as legal entities similar to companies.

In addition, international organizations have made specific recommendations regarding the unique nature of the DeFi market to minimize financial stability risks. The Financial Stability Board and the Organization for Economic Cooperation and Development stress the importance of constant monitoring of Defi’s development and stringent prevention of its spillover risks. The International Organization of Securities Commissions requires key participants with significant control of or impact on DeFi arrangements to resolve conflict of interests, major risks, and disclosure-related problems. Since DeFi is still in its infancy, there have been few regulations targeting DeFi activities. A relevant example is the “DLT Foundations Regulations 2023” introduced by the Financial Services Registration Authority of the Abu Dhabi Global Market in 2023, consisting of provisions related to DeFi.

The Hong Kong SAR Government embraces the legitimacy of virtual assets and their role in the financial sector. Service providers are welcome to establish operations here, ensuring they have timely and necessary preventive measures in place. According to Mr Enoch Fung, CEO of the Hong Kong Academy of Finance, emerging technologies related to DeFi and the metaverse, which are inextricably linked to the growth of virtual assets and Web 3.0, are likely to bring opportunities to the financial services industry. To market participants, a clear regulatory framework, powerful financial infrastructure and networks, and people with blockchain-related skills are crucial to the future prospects of DeFi and the virtual-asset market in Hong Kong.

【Note 1】 Hong Kong Institute for Monetary and Financial Research. “Decentralised Finance: Current Landscape and Regulatory Developments”. HKIMR Applied Research Report No.1/2024.

【Note 2】 Aramonte, S., Huang, W., & Schrimpf, A. (2021). “DeFi risks and the decentralisation illusion”. BIS Quarterly Review.

Dr. Maurice K.S. Tse

Principal Lecturer in Finance

Ms. Vivian Cheung

HKU SPACE College Senior Lecturer

Mr. Clive Ho

HKU SPACE College Lecturer

(This article was also published on July 24, 2024 in the “Lung Fu Shan” column of the Hong Kong Economic Journal)